|

|

|

|

|

|

|

|

|

|

|

|

Concept of Mutual Fund

|

|

|

|

|

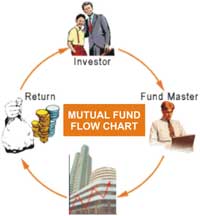

| The flow chart below describes

broadly the working of a mutual fund: |

| |

| How does a Mutual fund work? |

| A mutual fund is a collection

of stocks, bonds, or other securities owned by a group of investors

and managed by a professional investment company. For an individual

investor to have a diversified portfolio is difficult. But he can

approach to such company and can invest into shares. Mutual funds

have become very popular since they make individual investors to

invest in equity and debt securities easy. When investors invest

a particular amount in mutual funds, he becomes the unit holder

of corresponding units. In turn, mutual funds invest unit holders

money in stocks, bonds or other securities that earn interest or

dividend. This money is distributed to unit holders. If the fund

gets money by selling some stocks at higher price the unit holders

also are liable to get capital gains. A mutual fund is quite simply

a collection of stocks, bonds, or other securities owned by a group

of investors and managed by a professional investment company.

Thus the mutual funds are not the depositing instrument that has

guarantee of getting certain amount but it is like any other securities

where the investor can have capital gains or loss. |

|

|

| Advantages of Mutual Fund |

Professional Management - The primary

advantage of funds (at least theoretically) is the professional

management of your money. Investors purchase funds because they

do not have the time or the expertise to manage their own portfolio.

A mutual fund is a relatively inexpensive way for a small investor

to get a full-time manager to make and monitor investments.

Diversification - By owning shares in a mutual fund

instead of owning individual stocks or bonds, your risk is

spread out. The idea behind diversification is to invest in

a large number of assets so that a loss in any particular investment

is minimized by gains in others. In other words, the more stocks

and bonds you own, the less any one of them can hurt you (think

about Enron). Large mutual funds typically own hundreds of

different stocks in many different industries. It wouldn't

be possible for an investor to build this kind of a portfolio

with a small amount of money.

Economies of Scale - Because a mutual fund buys and sells

large amounts of securities at a time, its transaction costs

are lower than you as an individual would pay.

Liquidity - Just like an individual stock, a mutual fund

allows you to request that your shares be converted into cash

at any time.

Simplicity - Buying a mutual fund is easy! Pretty well

any bank has its own line of mutual funds, and the minimum investment

is small. Most companies also have automatic purchase plans whereby

as little as Rs 1000 can be invested on a monthly basis. - |

|

| History of Mutual Fund in India |

- Pioneer of mutual fund is UTI in 1963.

- Actual growth started in 1987.

- The dramatic improvement through quality wise and quantity

wise.

- Main reason for its poor growth is new concept in the

country.

- Large sections of Indian investor are yet to be intellectual

with this concept.

- Hence the it is prime responsibility of all Mutual Fund

companies , to make the product correctly abreast of selling.

- There are four 4 phases according to the development of

sector

|

|

| First Phase 1964-1987 |

- 1964 to 1987: - Unit Trust of India (UTI) was established

on 1963 by an Act of Parliament.

- It was set up by the Reserve Bank of India and functioned

under the Regulatory and administrative control of the Reserve

Bank of India.

- In 1978 UTI was de-linked from the RBI and the Industrial

Development Bank of India (IDBI) took over the regulatory

and administrative control in place of RBI.

- The first scheme launched by UTI was Unit Scheme 1964.

At the end of 1988 UTI had Rs.6,700 cores of asset

|

| Second Phase –

1987-1993 (Entry of Public Sector Funds) |

- 1987 marked the entry of non- UTI, public sector mutual funds

set up by public sector banks and Life Insurance Corporation

of India (LIC) and General Insurance Corporation of India (GIC).

- SBI Mutual Fund was the first non- UTI Mutual Fund established

in June 1987 followed by Canbank Mutual Fund (Dec 87), Punjab

National Bank Mutual Fund (Aug 89), Indian Bank Mutual Fund

(Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund

(Oct 92).

- LIC established its mutual fund in June 1989 while GIC

had set up its mutual fund in December 1990.

- At the end of 1993, the mutual fund industry had assets

under management of Rs.47,004 crores.

|

|

| Third Phase –

1993-2003 (Entry of Private Sector Funds)

|

- With the entry of private sector funds in 1993, a new era

started in the Indian mutual fund industry, giving the Indian

investors a wider choice of fund families. Also, 1993 was the

year in which the first Mutual Fund Regulations came into being,

under which all mutual funds, except UTI were to be registered

and governed.

- The erstwhile Kothari Pioneer (now merged with Franklin Templeton)

was the first private sector mutual fund registered in July 1993.

- The 1993 SEBI (Mutual Fund) Regulations were substituted by

a more comprehensive and revised Mutual Fund Regulations in 1996.

The industry now functions under the SEBI (Mutual Fund) Regulations

1996.

- The number of mutual fund houses went on increasing, with many

foreign mutual funds setting up funds in India and also the industry

has witnessed several mergers and acquisitions.

- As at the end of January 2003, there were 33 mutual funds with

total assets of Rs. 1,21,805 crores.

- The Unit Trust of India with Rs.44,541 crores of assets under

management was way ahead of other mutual funds.

|

|

| Fourth Phase – since February 2003 |

- In February 2003, following the repeal of the Unit

Trust of India Act 1963 UTI was bifurcated into two separate

entities. One is the Specified Undertaking of the

Unit Trust of India with assets under management of Rs.29,835

crores as at the end of January 2003, representing broadly,

the assets of US 64 scheme, assured return and certain other

schemes.

- The Specified Undertaking of Unit Trust of India, functioning

under an administrator and under the rules framed by Government

of India and does not come under the purview of the Mutual Fund

Regulations.

- The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB,

BOB and LIC. It is registered with SEBI and functions under the

Mutual Fund Regulations

- With the bifurcation of the erstwhile UTI which had in March

2000 more than Rs.76,000 crores of assets under management and

with the setting up of a UTI Mutual Fund, conforming to the SEBI

Mutual Fund Regulations, and with recent mergers taking place

among different private sector funds, the mutual fund industry

has entered its current phase of consolidation and growth.

The graph indicates the growth of assets over the years.

|

|

| Growth in Asset Under Management |

|

| |

| Regulations |

| Mutual Funds in India are governed by the SEBI

(Mutual Fund) Regulations 1996 as amended from

time to time. For further details please visit the SEBI website http://www.sebi.gov.in |

| |

| Organization of Mutual Fund |

|

| |

|

| The structure consists of |

Sponsor is the person who acting alone or in combination with another

body corporate establishes a mutual fund. Sponsor must contribute

at least 40% of the net worth of the Investment Managed and meet

the eligibility criteria prescribed under the Securities and Exchange

Board of India (Mutual Funds) Regulations, 1996.The Sponsor is

not responsible or liable for any loss or shortfall resulting from

the operation of the Schemes beyond the initial contribution made

by it towards setting up of the Mutual Fund.

The Mutual Fund is constituted as a trust in accordance with

the provisions of the Indian Trusts Act, 1882 by the Sponsor.

The trust deed is registered under the Indian Registration

Act, 1908.

Trustee is usually a company (corporate body) or a Board of Trustees

(body of individuals). The main responsibility of the Trustee

is to safeguard the interest of the unit holders and inter

alias ensure that the AMC functions in the interest of investors

and in accordance with the Securities and Exchange Board of

India (Mutual Funds) Regulations, 1996, the provisions of the

Trust Deed and the Offer Documents of the respective Schemes.

At least 2/3rd directors of the Trustee are independent directors

who are not associated with the Sponsor in any manner.

The Trustee as the Investment Manager of the Mutual Fund appoints

the AMC. The AMC is required to be approved by the Securities

and Exchange Board of India (SEBI) to act as an asset management

company of the Mutual Fund. Atlas 50% of the directors of the

AMC is an independent director who is not associated with the

Sponsor in any manner. The AMC must have a net worth of at

least 10 crore at all times.

The AMC if so authorized by the Trust Deed appoints the Registrar

and Transfer Agent to the Mutual Fund. The Registrar processes

the application form; redemption requests and dispatches account

statements to the unit holders. The Registrar and Transfer

agent also handles communications with investors and updates

investor records. |

| |

|

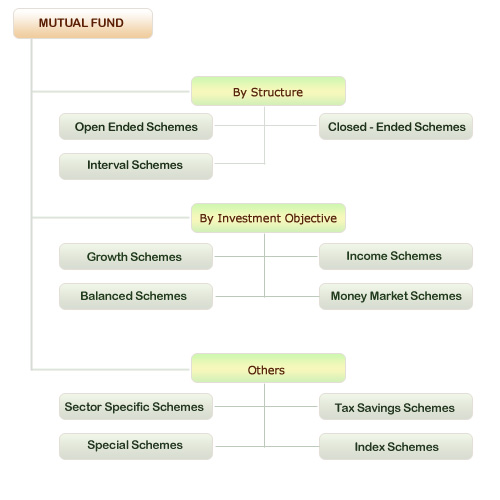

| Types of Mutual Fund |

|

Equity Oriented Schemes

These schemes, also commonly called Growth Schemes, seek to invest

a majority of their funds in equities and a small portion in money

market instruments. Such schemes have the potential to deliver

superior returns over the long term. However, because they invest

in equities, these schemes are exposed to fluctuations in value

especially in the short term.

Equity schemes are hence not suitable for investors seeking regular

income or needing to use their investments in the short-term. They

are ideal for investors who have a long-term investment horizon.

The NAV prices of equity fund fluctuates with market value of the

underlying stock which are influenced by external factors such

as social, political as well as economic. |

| |

Index Schemes

Index Funds replicate the portfolio of a particular index such

as the BSE Sensitive index, S&P NSE 50 index (Nifty), etc

These schemes invest in the securities in the same weight age

comprising of an index. NAVs of such schemes would rise or fall

in accordance with the rise or fall in the index, though not

exactly by the same percentage due to some factors known as "tracking

error" in technical terms. Necessary disclosures in this

regard are made in the offer document of the mutual fund scheme.

There are also exchange traded index funds launched by the mutual

funds, which are traded on the stock exchanges. |

| |

Sector Specific Schemes

These are the funds/schemes, which invest in the securities of

only those sectors or industries as specified in the offer documents.

e.g. Pharmaceuticals, Software, Fast Moving Consumer Goods (FMCG),

Petroleum stocks, etc. The returns in these funds are dependent

on the performance of the respective sectors/industries. While

these funds may give higher returns, they are more risky compared

to diversified funds. Investors need to keep a watch on the performance

of those sectors/industries and must exit at an appropriate time.

They may also seek advice of an expert.

|

| |

Tax Saving Schemes

These schemes offer tax rebates to the investors under specific

provisions of the Income Tax Act, 1961 as the Government offers

tax incentives for investment in specified avenues. e.g. Equity

Linked Savings Schemes (ELSS). Pension schemes launched by the

mutual funds also offer tax benefits. These schemes are growth

oriented and invest pre-dominantly in equities. Their growth

opportunities and risks associated are like any equity-oriented

scheme.

|

| |

Income/Debt Oriented

Scheme

The aim of income funds is to provide regular and steady income

to investors. Such schemes generally invest in fixed income securities

such as bonds, corporate debentures, Government securities and

money market instruments. Such funds are less risky compared to

equity schemes. These funds are not affected because of fluctuations

in equity markets. However, opportunities of capital appreciation

are also limited in such funds. The NAVs of such funds are affected

because of change in interest rates in the country. If the interest

rates fall, NAVs of such funds are likely to increase in the short

run and vice versa. However, long term investors may not bother

about these fluctuations.

|

| |

Hybrid/Balanced

Schemes

These schemes are commonly known as balanced schemes. These schemes

invest in both equities as well as debt. By investing in a mix

of this nature, balanced schemes seek to attain the objective of

income and moderate capital appreciation and are ideal for investors

with a conservative, long-term orientation. Balanced Fund and Gift

Fund are examples of hybrid schemes. |

| |

Money Market/Liquid Schemes

These funds are also income funds and their aim is to provide easy

liquidity, preservation of capital and moderate income. These schemes

invest exclusively in safer short-term instruments such as treasury

bills, certificates of deposit, commercial paper and inter-bank

call money, government securities, etc. Returns on these schemes

fluctuate much less compared to other funds. These funds are appropriate

for corporate and individual investors as a means to park their

surplus funds for short periods.

|

| |

Gilt Schemes

These funds invest exclusively in government securities. Government

securities have no default risk. NAVs of these schemes also fluctuate

due to change in interest rates and other economic factors as

are the case with income or debt oriented schemes. |

| |

Arbitrage Fund

Arbitrage is one of the most effective ways to insulate against

market volatility. An arbitrage fund buys equities in the cash

market and simultaneously sells in the futures market, thus ensuring

market neutrality for the investment. In

other words, it is a unique asset class by itself where returns

are generated by capturing the pricing differential between the

cash and the futures markets. It is also termed as a market-neutral

fund where the returns are not going to be impacted by volatility

in the market.

For any arbitrage fund, the following market conditions are beneficial -- a bullish market and a volatile

market. While the

fund performs very well in bullish markets, a volatile market gives

it opportunities for early exit, thus enhancing the overall yield

of the portfolio. However, a prolonged bear phase is not an ideal

situation for this kind of product. |

| |

Difference between Arbitrage

Fund & Income Fund both in terms of risk and returns

In terms of returns, an arbitrage fund is better than an income

product. An income product has a fixed yield-to-maturity while

in an arbitrage product, the yields are better due to lower cost

of carry and are usually in the range of 10-14%.

Secondly, the risk parameters are similar or lower than an income

product. An arbitrage fund does not

carry any credit rating risk and interest rate risk, while the

returns can be much higher than an income product. Added to this,

a mutual fund arbitrage product enjoys all the tax benefits enjoyed

by mutual fund products

Derivatives in India have more often been used for speculation

purposes than for hedging and arbitrage. What are your views on

this?

Both in India and the world over, derivatives have been widely

used as a leverage product but as the trends are changing and the

investors are maturing, the other tools like hedging and risk free

arbitrage strategies are also being widely used. |

| |

Gold Exchange-Traded

Schemes

Exchange-traded funds (ETFs) are mutual fund schemes that are listed

and traded on exchanges like stocks. ETFs trading value is based

on the net asset value (NAV) of the assets it represents. Generally,

ETFs invest in a basket of stocks and try to replicate a stock

market index such as the S&P CNX Nifty or BSE Sensex, a market

sector such as energy or technology, or a commodity such as gold

or petroleum.

Recently, the Securities and Exchange Board of India (SEBI) amended

its regulations and allowed mutual funds launch gold exchange-traded

funds (GETFs) in India. Two mutual funds, UTI mutual fund and Benchmark

Mutual Fund, has been launched. These funds got listed on

the National Stock Exchange (NSE).

A gold-exchange traded fund unit is like a mutual fund unit backed

by gold as the underlying asset and would be held mostly in demat

form. An investor would get a securities certificate issued by

the mutual fund running the Gold-ETF defining the ownership of

a particular amount of gold. GETFs are designed to offer investors

a means of participating in the gold bullion market without the

necessity of taking physical delivery of gold, and to buy and sell

through trading of a security on a stock exchange.

With gold being one of the important asset classes, GETFs will

provide a better, simpler and affordable method of investing as

compared to other investment methods like bullion, gold coins,

gold futures, or jewelry.

|

Maturity Plans (FMPs)

Safe, predictable and better post-tax returns than bank FDs

Rising interest rates not only mean rising EMIs but also offer

an opportunity to earn higher returns. Debt schemes are now offering

attractive returns with short-term rates in the region of 8-10%.

Call money rates have been moving higher to about 7.5-8% due to

tight liquidity conditions. With the RBI deciding to raise the

cash reserve ratio (CRR), liquidity conditions have worsened. Tightness

in the money markets is expected to continue till the end of the

current financial year and investors can consider investing in

short term options like FMPs or floating rate schemes. Fixed

maturity plans, or FMPs as they are popularly called, are close-ended

funds with a fixed tenure and invest in a portfolio of debt products

whose maturity coincides with the maturity of the product.

The primary objective of a FMP is to generate income while protecting

the capital by investing in a portfolio of debt and money market

securities. The tenure can be of different maturities, ranging

from one month to five years.

FMPs can be compared to fixed deposits of a bank. While a fixed

deposit offers a 'guaranteed' return, returns in FMPs are only

'indicative'. Typically, the fund house fixes a 'target amount'

for a scheme, which it ties up informally with borrowers before

the scheme opens. That way it knows the interest rate it will earn

on its investments, providing the 'indicative return' to investors. |

| |

Monthly Income Plans

Monthly income plans, or MIPs, as they are more popularly known,

are a category of mutual funds that invest mainly in debt instruments.

Only about 10-20-% of the assets are allocated to equity

stocks. But the very name – monthly

income plan – is a misnomer, as these funds do not guarantee

a monthly income. Like any other fund, the returns are market-driven.

Though many fund houses strive to declare a monthly dividend, they

have no such obligation. MIPs are launched with the objective of

giving a monthly income to investors, but the periodicity depends

upon the option chosen by the investor. These are generally monthly,

quarterly, half-yearly and annual options. A growth option is also

available, where the investors do not receive regular dividends,

but gains in the form of capital appreciation. |

|

|